Market Barriers to the introduction of medical devices in Germany. What could these be and how can they be overcome?

Market barriers to market entry in Germany for Medical Device Manufacturers

December 2020, Maria Klaas – According to a recent study from 2020 by Clairfield International, the German medical technology market is by far the largest in Europe with € 33 billion. It is therefore no wonder that small and medium-sized enterprises (SMEs) from Germany or abroad want to participate in this market.

Market Barriers in Germany

Attractive markets offer interesting market potential, but can also include obstacles, market barriers. The medical technology market already holds such barriers due to its structure. What are or could be these market barriers?

The very first market barrier is the CE mark. Only products that are CE certified can be introduced throughout Europe. The fact that the new MDR (Medical Device Regulation), which will take effect from May 2021, is delaying CE certification is not only due to the regulations, but currently precisely due to the limited number of Notified Bodies. If an SME deals with medical devices, this is known and we will not go into it further here.

What barriers do SMEs now face that are in position ready for the market?

We have identified the following barriers in recent years:

(1) Health reimbursement

(2) Product Acceptance

(3) Market power of suppliers

(4) Segment communities

(5) Product quality

(1) Market Barrier – Health reimbursement

First of all, there is the health reimbursement as the strongest market barrier in Germany.

With a few exceptions, almost all inhabitants of Germany have health insurance – 10% belong to private insurance and 90% to statutory insurance. If the SME has a medical product that is reimbursable through health insurance, it should take a close look at this system. Under certain circumstances, it could otherwise lose very good sales opportunities.

After the product has been positioned segment-specifically, a health reimbursement analysis should be carried out according to this positioning. Several reimbursement systems exist in Germany.

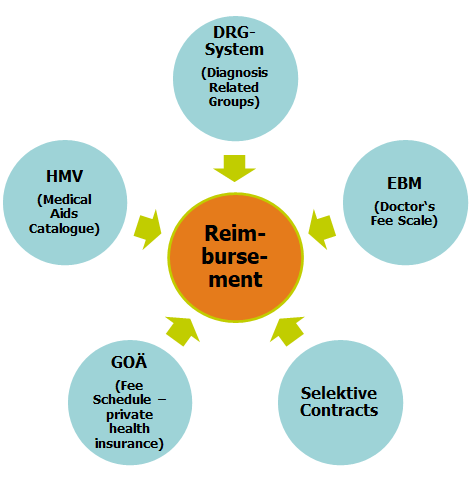

Outpatient Sector

For example, in the outpatient sector, there is billing according to EBM for medical care for those with statutory health insurance and according to GOÄ for those with private health insurance, as well as the catalogue of medical aids to make medical aids (e.g. wheelchairs, support stockings) reimbursable.

Inpatient Sector

Everything that is to be paid for in the inpatient sector, as in hospitals, is billed according to DRG in Germany and additionally calculated according to GOÄ for privately insured persons.

Typical hospital product examples: Implants, professional wound care, etc.

In addition, selective contracts can still be mentioned. You will find an overview below.

Health reimbursement in Germany is a very complex issue. It is definitely worth consulting a business consultant for this. He can find out whether the medical product already has access to the health reimbursement system.

If not, the SME will receive recommendations on what to do and how to generate sales – or whether it would not be better to place the medical product in the self-pay segment.

In addition, the SME receives valuable information on the required studies, which could possibly be combined with the necessary studies for a pending CE certification. Therefore, in the case of high classifications, please be sure to obtain this knowledge before or during CE certification.

(2) Market Barrier – Product acceptance

Another market barrier in Germany could simply be that the medical device is not needed / accepted in the market.

Reasons e.g.:

– The product does not correspond to the habits of the users, e.g. the surgical gown is offered too short, as surgeons in the country of manufacture operate in a sitting position and not standing as is customary in Germany.

– The group of medical products is intended for a high end price segment. For the market, the conventional “cheaper” products are good enough. Although the product advantages are obvious, the user/buyer is not willing to pay more. e.g. IV cannulas.

However, if the quality requirements are raised by legislation, as happened a few years ago with safety cannulas, higher prices can be enforced.

Users or opinion leaders can provide useful information on this. Competitor/user surveys at trade fairs are usually sufficient to obtain a good assessment.

(3) Market power of suppliers:

Some product areas are dominated by only a few offering medical technology manufacturers. This may be because there are simply only these manufacturers or because the type of medical product only allows a certain choice of distribution channels.

A typical example was the diabetes sector more than 15 years ago. Only as a result of health structure laws passed by the federal government has this now also become accessible to many other providers.

Another example is the product segment of compression stockings, where well-known German manufacturers have created a second certification hurdle for competitors, the RAL quality mark, as a seal of quality for compression stockings.

Possible solutions are offered by an innovative product and niche strategy. Create unique product features and use niche suppliers as strategic partners. A differentiated distribution channel strategy can also be promising.

(4) Segment communities:

The more specialised and smaller a market segment is, the smaller the community.

For example, the cardio or spine or diabetes sectors are very small communities. If someone is employed in these areas, he will stay there. The main reason is certainly to be found in the acquired specialised knowledge with additional professional qualifications. But also the good contacts to customers/doctors that have been built up over many years – people speak at eye level. For external SME newcomers/start-ups, this is an almost insurmountable barrier.

It is recommended to work with a strategic sales partner or with a management consultant who belongs to these communities or has contacts to the market participants through previous professional experience. In the case of a direct sales strategy via one’s own sales force, good contacts to these communities should be a matter of course as the main selection criterion. Contacts are the be-all and end-all here.

(5) Product quality:

The product quality must meet the requirements of the German market and the customers. These are shaped by national circumstances, traditions, religions, mentalities – to name but a few.

In Germany, the technical characteristics of a product are often not enough. For some target groups, the product design must also meet ethical needs. For example, a laser used by a dermatologist or in beauty medicine would not be bought for its technical advantages if the design was neglected in terms of taste.

The service component suitable for products requiring explanation or highly technical/electronic products should round off the offer.

With a clear differentiation from the competition, SMEs have the best market entry strategy. A good aid is provided by a SWOT analysis, which clearly presents all the components of the target group previously collected in a market analysis and provides valuable information on the “right” quality.

To sum up:

Depending on the product and target group orientation, there are low or high market barriers for SMEs. Please do not be discouraged. With the collection of detailed information during market research or analysis, demonstrated creativity, combined with a willingness to take risks, market entry in Germany will be successful. That’s for sure!

Read also

“Efficiency increase of the strategic distribution of medical devices in Europe for SMEs”